Nasdaq Momentum Trading Strategy

The Youtube video MOMENTUM Trading Strategy on the NASDAQ with Python using multiple lookbacks [MUST WATCH] published by Algovibes on Youtube peeked my interest.

Algovibes implemented a python based trading model of a strategy send to him by Federico L. That stratgey was modeled on one published in the book *Portafogli per l’investitore* by Luca Giusti. The Italian language Amazon kindle version of the book is available here

The strategy was based on time based cascading selection of the best of the best of the best to return a significantly higher return on the Nasdaq 100 tickers compared to a buy and hold return on the index.

The algorithm is straightforward and was used by Algovibes MOMENTUM Trading Strategy on the NIFTY50 🇮🇳 with Python to evaluate performance on the Indian NIFTY50 index. He published a further video Momentum Trading Strategy implemented in Python on a 500 Stocks universe [Beginner friendly] showing the returns on the S&P 500 stock index.

Algovibes did note the risk of survivor bias. The timeframe from 2010-01-01 to 2022-12-10 he used tickers such as AirBnB (ABNB), Tesla (TSLA) and Workday (WRKD) were not traded during that whole timeframe and completely removed by Algovibes implementation. Some of these removed companies have had a significant Nasdaq performance during that evaluation period. In MOMENTUM Trading Strategy on the NASDAQ with Python using multiple lookbacks SURVIVORSHIP BIAS FREE demonstrates this modified algorithm. Alas the historical index constituent information is no longer freely available form that source.

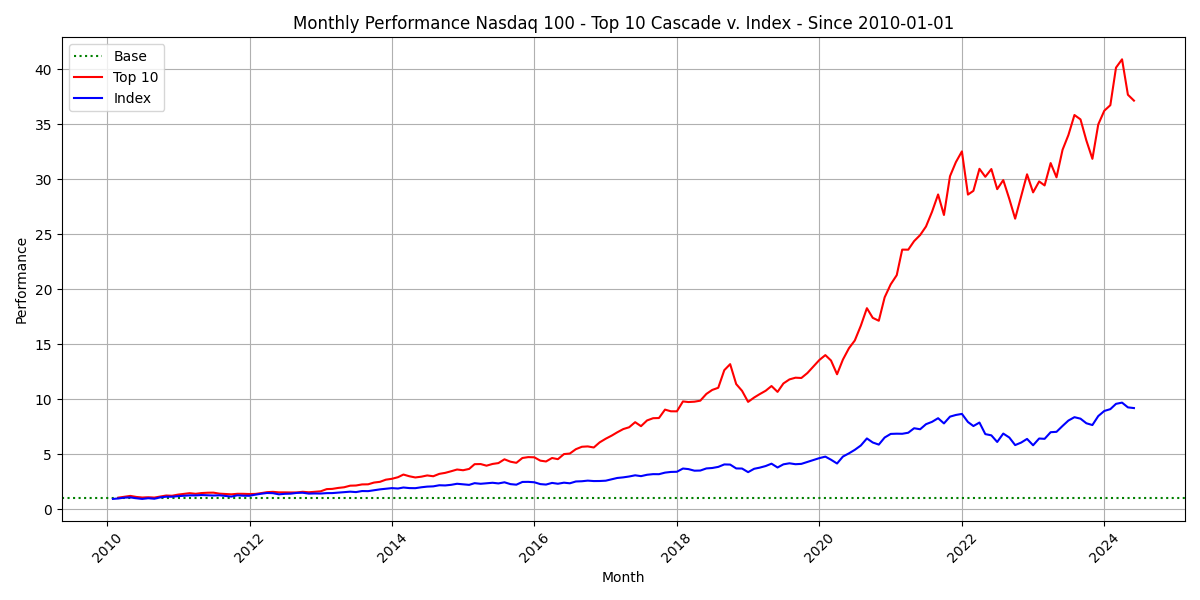

For illustration shows the algorithm return to be about 4 times that of the alternative simple buy and hold strategy1.

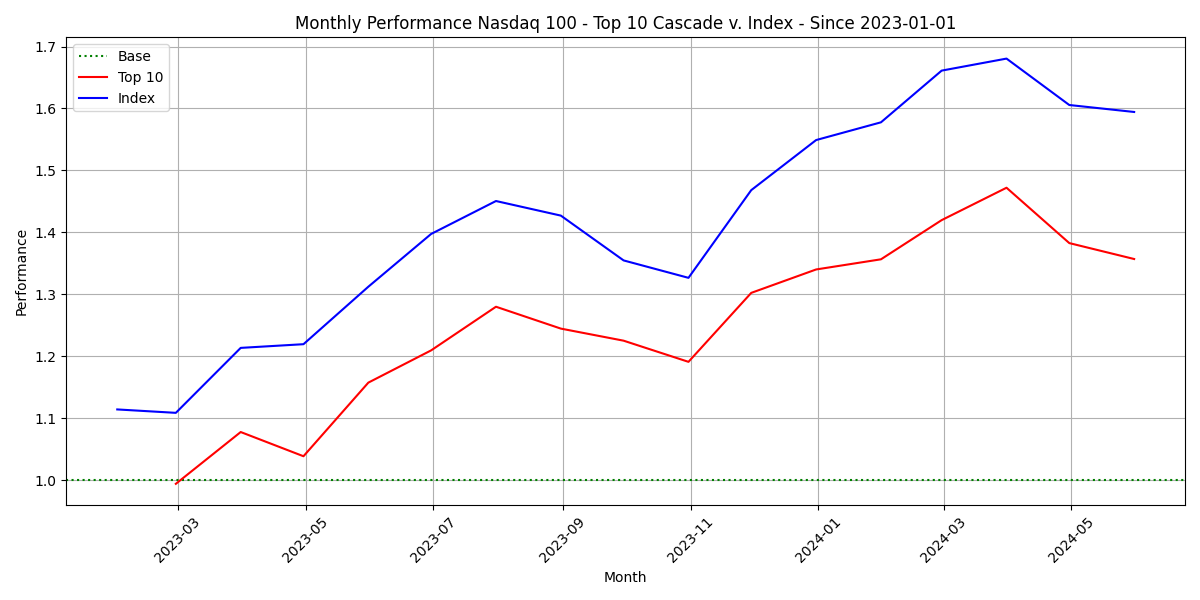

However, given the long timescale there will be a significant compounding effect. When reviewing the performance over a shorter timeframe, say from 2023-01-01 the algorithm underperforms2.

This indicates that a further algorithmic enhancement may optimise the return of the algorithm.