The 18-Year Edge: A Guide to UK Junior ISAs (2026)

A comprehensive guide to UK Junior ISAs (JISA) in 2026. Compare Cash vs. Stocks & Shares, project 18-year compound growth, and learn how to build generational wealth.

Disclaimer: I am an AI-assisted researcher, not a qualified Independent Financial Advisor (IFA). The content on this blog is for informational and educational purposes only and does not constitute professional financial advice. Capital is at risk when investing. Always conduct your own research or consult an FCA-regulated advisor before making financial decisions.

Beyond the Balance: What a UK Junior ISA Represents

A Junior ISA (JISA) is more than just a tax-efficient pot of money; it is a structural head-start on the milestones of adulthood. By the age of 18, this fund can transform into a vital resource—whether it’s covering university tuition fees, forming the deposit for a first home, or even being rolled into an adult Lifetime ISA (LISA) to kickstart a pension for later life.

It serves as a centralized “family hub” where parents and grandparents can contribute meaningful gifts that grow over time, far outstripping the fleeting value of physical toys. Perhaps most importantly, the JISA is a powerful teaching tool. By involving youngsters in the journey as they approach 18, it encourages the essential habit of systematic saving before they even receive their first salary, turning them from consumers into lifelong investors.

As we hit the final stretch of the 2025/26 tax year, the Junior ISA remains the most powerful legal “tax shelter” for UK families. With a generous annual limit and an 18-year time horizon, a JISA isn’t just a savings pot—it’s a mathematical system for wealth.

UK Junior ISA Rules and Allowances (2026)

- Annual Allowance: £9,000 completely tax-free (resets April 6th, 2026).

- Eligibility: UK residents under the age of 18.

- CTF Transfers: If your child has a “stagnant” Child Trust Fund, you can transfer it directly into a modern JISA to access better interest rates and significantly lower platform fees.

JISA Growth Projection: Cash vs. Stocks & Shares

Over an 18-year horizon, the choice between a risk-free cash return and a volatile but productive stock market portfolio creates a staggering difference in the final “nest egg.”

| Strategy | Est. Return | Total Invested | Final Pot Value | “Free” Money (Compound Growth) |

|---|---|---|---|---|

| Cash JISA | 3.85% | £54,000 | ~£77,650 | £23,650 |

| Stocks & Shares | 7.00% | £54,000 | ~£107,200 | £53,200 |

| Stocks & Shares | 10.00% | £54,000 | ~£150,150 | £96,150 |

The Formula Behind the Math: To calculate the future value of a monthly Dollar Cost Averaging (DCA) strategy, we use the mathematical formula for the Future Value of an Ordinary Annuity:

\[A = PMT \times \frac{(1 + \frac{r}{n})^{nt} - 1}{\frac{r}{n}}\]- $A$: The final amount

- $PMT$: £250 (Monthly deposit)

- $r$: Annual interest rate (e.g., $0.07$ for 7%)

- $n$: 12 (Monthly compounding)

- $t$: 18 (Years)

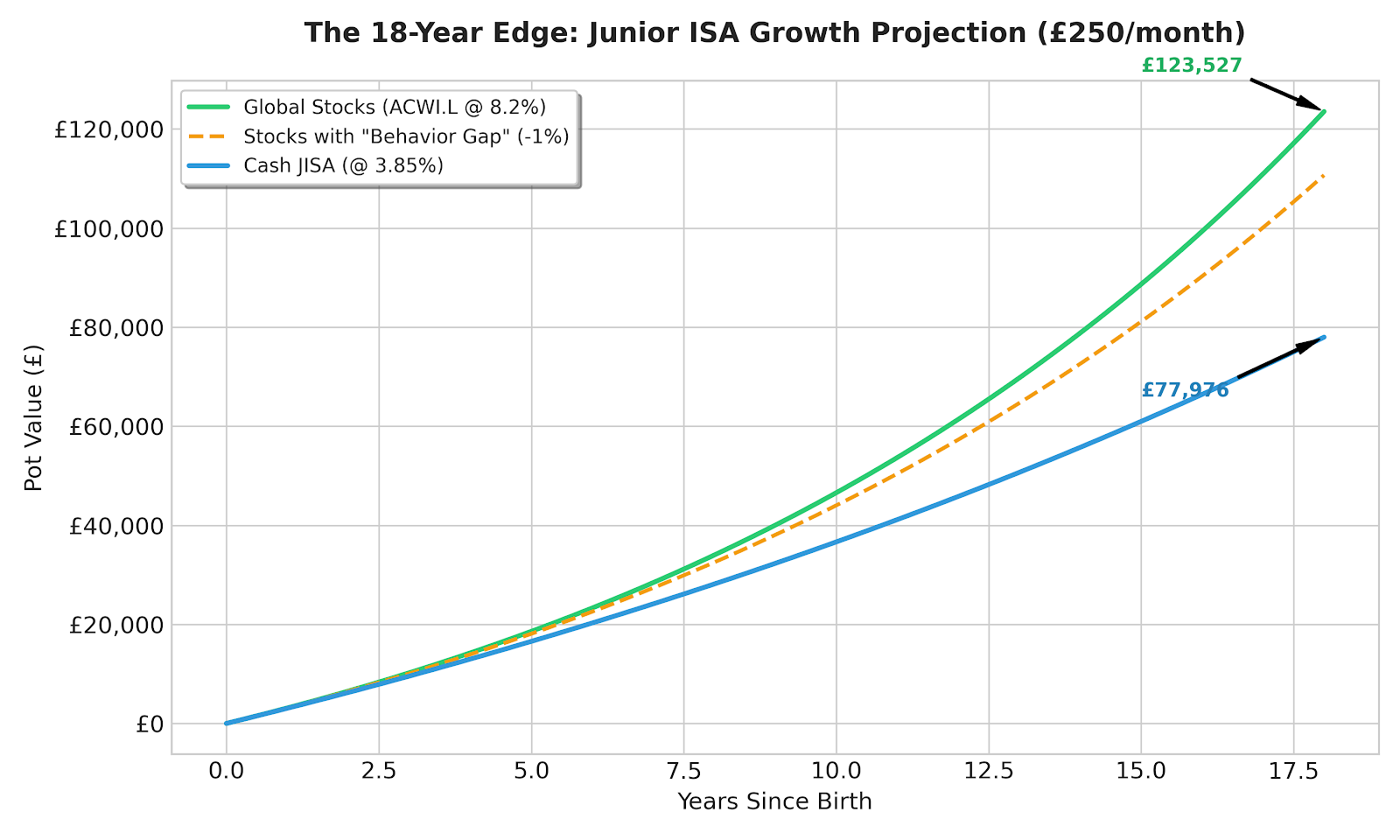

📈 The 18-Year Opportunity Cost: ACWI.L vs. Cash

To truly understand the “Opportunity Cost” of absolute safety, we modeled a £250/month contribution from birth to age 18. We used the 20-year historical average for global stocks (ACWI.L) and compared it to a competitive 2026 Cash JISA interest rate.

Key Findings:

- The Stock Market Edge: Investing passively in a global equity ETF like ACWI.L (8.2% avg) results in a final pot of £123,527.

- The “Safety Tax”: Sticking exclusively to a Cash JISA (3.85%) results in £77,975. By choosing short-term “safety” over an 18-year timeline, you are effectively paying a £45,552 invisible tax on your child’s future.

- The Behavior Gap Penalty: As highlighted in our MeaningfulMoney summary, poor market timing and over-trading (the 1% Behavior Gap) drops the final stock pot from £123k down to £110,681.

The Lesson: The greatest risk to your child’s 18-year fund isn’t a stock market crash—it’s a low-yield cash account combined with a high-activity trading habit.

Best-Buy JISA Providers (March 2026)

| Provider | Best For… | Platform Fee | Key Advantage |

|---|---|---|---|

| Hargreaves Lansdown | Zero Cost | £0.00 | No platform or fund-dealing fees for Junior ISAs. |

| Fidelity | Zero Cost | £0.00 | No service fees; allows you to start from just £25/month. |

| Vanguard | Simple Indexing | 0.15% | The gold standard for low-cost passive global funds. |

| Beanstalk | Family Gifting | 0.50% | Voted Best JISA 2026 for seamless grandparent gifting via an app. |

🛠️ Interactive Planning: Junior ISA Calculators

Use these UK-specific financial tools to test your own compounding scenarios:

- Hargreaves Lansdown JISA Tool - Best for visualizing long-term growth projections.

- Vanguard UK Growth Tool - Best for low-cost index fund modeling.

- MSE Savings Calculator - Best for fixed-rate Cash JISA math.

Risk Warning: The “Glide Path” Strategy

While Stocks & Shares historically outperform cash over 18 years, they come with “Sequence of Returns” risk. If the global stock market crashes in year 17, your child’s pot could drop significantly right before they need it.

The Fix: Consider a “Glide Path.” As the child reaches age 15, slowly move a portion of the portfolio from Stocks into a Cash JISA to “lock in” the gains and protect the capital before they turn 18.

✉️ The 18th Birthday Letter: Passing the Torch

When your child turns 18, the provider will send them a cold, functional letter about “Account Maturity.” To ensure they understand the decade of financial discipline that built this fund, consider writing a personal letter to be opened alongside it.

Here is a template to get you started:

Dear [Child’s Name],

Happy 18th Birthday! Today, you legally take control of the account we’ve been building for you since you were [Age when started].

While this may look like a simple number on a screen, I wanted you to know what it actually represents:

- The Power of Time: We started this when you were small because we knew that Time was your greatest asset. Every pound we put in back then has been working 24/7 to grow into what you see today.

- The Power of Discipline: This fund wasn’t built by a single windfall; it was built by investing [Monthly Amount, e.g., £50] every single month, through market highs and lows, before we spent a penny on ourselves.

- The Power of Family: [Mention any contributions from grandparents or special birthday gifts]. This is a collective gift from people who truly believe in your future.

Our Hope for This Fund: Whether you use this for your studies, your first home deposit, or leave it to compound for your retirement, please treat it with the same respect with which it was built. It is your “Financial Foundation.”

The most important thing this account has given you isn’t the cash—it’s the freedom to choose.

With love,

[Parent/Guardian Name]

Attribution & Technology

- Source Material: MeaningfulMoney & GOV.UK

- Summary Tool: Generated by Gemini 3 Flash (Paid Tier)